India

India directs banks to operate during lockdown

India directs banks to operate during lockdown

This is to ensure that the government’s relief package reaches the poor.

Chart of the Week: India's retail loans will reach $566.7b in 2023

It reached a 17% CAGR to $319.1b in 2018.

Yes Bank, State Bank of India will not merge

The Indian central bank took over Yes Bank for not having enough capital.

HDFC bank appoints new Additional Non-Executive Director

Karnad has been associated with the property and mortgage industry for over 40 years.

India's shadow banks hit with $15.1b in debt repayments

Meeting the deadlines will be a challenge given the domestic funding crunch.

Huge returns boost foreign banks' investment in India

Foreign annualised ROEs grew 9.9% in the six months until end-September.

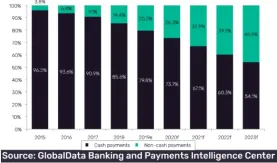

India's share of cash payments will lower to 54.1% by 2023

The government has waived merchant fees on payments through RuPay.

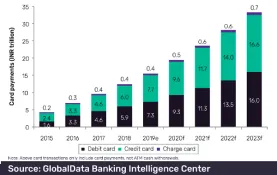

Indian card payments surge amidst cashless efforts

Total number of card payments quadrupled from 2 billion in 2015 to 7.8 billion in 2019.

Indian retail banks could claim bigger share of housing loan market in 2020

NBFCs and HFCs have reduced disbursement rates.

India's Religare Finvest may see 49% haircut with rare debt recast

Its lenders have reportedly agreed to write off almost half of its $808m debt.

Indian asset risks rise amidst NBFC funding stresses

The economy has grown dependent on non-bank lenders.

More Indian NBFCs to go overseas amidst funding crunch

Local funding remains constrained as providers pull back amidst a slowing economy.

India may slash benchmark rates by 25bps in February

High unemployment and a subued manufacturing sector will drive rate cuts.

Liquidity pressures to loom over India's NBFCs in 2020

Wholesale and housing finance companies are the most vulnerable.

Indian lender Yes Bank's bad loans swells by $457m

This is more than double the $174.86m the bank disclosed as of 30 September.

India's central bank chief calls for tighter scrutiny of state-run banks

RBI has limited sway over state-owned lenders, who control 60% of the banking sector.

Non-Performing Assets in India: An analysis over the years

The origination of the ongoing crisis of Non-Performing Assets (NPA) in India cannot be attributed to a single event nor can it be confined to a particular timeline. It was only in the mid 1990’s; post the economic liberalization when the country entered into the new millennium that the banks realized the sudden compounding of bad loans. The NPA situation essentially propelled in the mid 2000’s following over-optimism in the economy specifically between 2006-2008, on the back of strong economic growth and pending infrastructure projects completing on time and within specified budgets, a thing largely unheard-of till then. This irrational exuberance was followed by number of bad loans being advanced by the banks often by compromising due diligences. Riding on this positive environment, corporations were being granted loans based on recent performances and growth. Loans were being advanced at an alarming rate, and these corporations grew highly leveraged which led to most of the financing through external borrowings rather than internal equity. However, though post the global financial crisis of 2008, the bubbled economic growth stagnated and the repayment capability of the same corporations substantially decreased causing unparalleled financial stress on the banking and the corporate sectors. The strong projections for various projects started seeming unrealistic and it became increasingly clear there was no set structure in place to recuperate these loan advancements.

Thought Leadership Centre

In Association with

In Association with

Resource Center

Advertise

Advertise

Event News

New Charlton App ABF

It is a long established fact that a reader will be distracted by the readable content of a page when looking at its layout.