Singapore

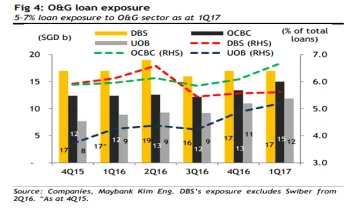

Chart of the Week: Singapore banks' lending to the O&G sector rose by as much as 20%

Chart of the Week: Singapore banks' lending to the O&G sector rose by as much as 20%

OCBC's exposure to the sector widened the most.

Asian banks brace for next wave of cyberattacks

Global cost of data breaches will reach an estimated $2.1t by 2019.

Why CASA deposits are no longer a cheap source of funding for Singapore banks

They've been paying up for such deposits to attract new customers.

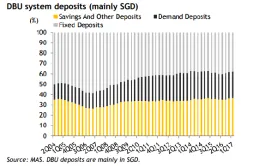

Chart of the Week: CASA deposits dominate Singapore banks' total customer deposits

Savings and demand deposits now comprise 62% of total deposits.

Weekly Global News Wrap Up: Why API strategy could define banking's future; Slowdown in financial globalisation could be cyclical

And EU warns Trump not to deviate from international banking rules.

How AI will dominate banking in Asia

Hillstone Networks, Latize, and Software AG Asia share why AI is the future of banking. Startup fintechs, e-commerce brands, and even established giants such as Google, Apple, Amazon, and Facebook are scrambling for their place in the money market, all driven by today’s rapidly evolving technology. This disruptive, game-breaking factor spoils consumers with convenience and intuitiveness in all facets of their life, and banks that fail to deliver just that will see their clients walking out the door. Fortunately, these alternative channels have not encroached that deeply into the traditional banking sector—yet. This gives banks a chance to step up their game, be more competitive, and hold their ground. Alan McIntyre, senior managing director and head of banking practice at Accenture, in their Banking Technology Vision 2017 report, explains, “The more goals a bank helps people achieve, the more confident people will be in the partnership, yielding an ever-stronger relationship with each interaction.” Reflecting the same sentiment is Anneliese Schulz, vice president of Software AG Asia. She says, “With the digital revolution changing the rules of banking, exceeding customer expectations is the key to growth and remaining competitive.” One way to achieve this is through trends such as artificial intelligence. Schulz explains this, saying, “Banks have to adopt a cohesive digital strategy by leveraging disruptive technologies such as AI to reimagine the customer experience and offer customers choices of where, when, and how they bank.” The AI experience “Elements of AI have been used in banking, finance, and insurance firms for quite some time now,” says Tim Liu, CTO of Hillstone Networks. “Backed by machine learning and big data, AI can automate tasks previously done by humans to help us make better, more informed decisions.” These machine learning systems will drive AI applications towards the ease of interaction customers are craving for. Better yet, the longer they run and the more they gain experience from data, the more effective they will be in addressing various banking situations, streamlining processes, and supporting customers. As it stands though, banks have only played on the fringes of AI’s full potential. Vikram Mengi, co-founder and CEO of Latize, says that it’s a huge missed opportunity. The data is there already, but “the problem with this is that the data is not necessarily in a form that can be easily utilised. However, by infusing the data with intelligence, one can transform all that data into a form that is easily usable.” Mengi sees the true success of AI in banking when these three aspects have been realised: a single knowledge base unifying all relevant diverse data sets; utilising knowledge representation models to interrogate known facts and infer unknown truths; and using abstraction layers through continuous application and learning from diverse data sets. “Banks have access to vast amounts of data and practical alignment of the above mentioned three aspects will result in value generation for banks and conversely the customers they’re serving,” he adds. In fact, 79% of banks surveyed in the Accenture report agree that AI will drastically improve their whole business and client relationships. Twenty-nine percent agree that it is critical for their products and services to be offered using centralised platforms, virtual assistants, and chatbots. Moreover, 76% foresee that most banks will have AI interfaces as their main customer touch points in the next three years, whilst a surprising 71% of them agree that AI can be the face of their business. To further emphasise how fast technology is evolving, it’s important to note that this AI-first mindset is quickly overtaking the relatively young mobile-first movement. Fitting into the puzzle “Moving forward, there are a number of areas in the industry where the implementation of AI can help streamline and improve processes,” says Liu. He notes areas like customer-facing functions and targeted marketing as two areas where AI can make an immediate, noticeable impact. Customer-facing functions involve the aforementioned robo-advisers, virtual assistants, and chatbots. In using AI applications for these services, “customer service can take a giant leap forward by eliminating the frustrating waiting time we are accustomed to,” says Liu. “Poor performance in this area is also a reason many internet banks have difficulty scaling up. Banks have adopted automated response systems for customer service and the system has improved over the years.” Besides being efficient time-wise, AI also frees customer service agents to focus more on complex situations where machines can’t match human empathy and intuition. Besides providing advice without human intervention, Schulz comments that the endeavor results in cost savings. “The key advantage of robo-advisers is that customers receive investment advice based on algorithm-based formula at a fraction of the cost of traditional financial advisors.” She adds, “Banks will see more automation and consolidation in asset management through the adoption of robo-advisors to improve customer experience. Eight in 10 consumers in Singapore would welcome robo-advisory services for their banking, insurance, and retirement planning according to a study by Accenture.” Banks can also implement AI to better bring customers the products and services that fit their needs. Liu says that after all, BFSIs do have the transactional and personal data necessary to determine the spending patterns and financial health of their clients. “Based on personal and demographic data, the system can identify opportunities and patterns previously unidentifiable by the human eye. This helps to better profile and therefore personalise marketing efforts to consumers, enabling prompt decision-making on marketing efforts to maximise impact and returns.” Schulz also points out that investments banks are researching how predictive analytics and machine learning can improve profitability through providing assisted decision-making in the sales and trading departments. “Banks are learning how to effectively use predictive analytics and machine learning to monetise customer data to create new capital from data sources and ultimately transform their business models,” she explains. In addition, Mengi says that AI can better secure the banking environment through anti-money laundering and anti-fraud measures. Going back to the amount of data banks have, they can “sift through it to spot irregularities and patterns that point to money laundering activity instead of just looking for anomaly and irregular pattern detection based on statistical methods.”

Meet Citi's new global subsidiaries group head for Asia Pacific

Find out how Munir Nanji plans to leverage the growth in intra-Asia trade.

Singapore banks have some scope to improve liability management: analyst

Banks are already working on lowering their liability cost.

JPMorgan launches Cross-Currency Sweeps, Just-in-Time Funding

Both are first-of-its-kind solutions for treasurers.

Weekly Global News Wrap Up: US banks launch mobile payments network; Qatari banks to boost deposit rates

And find out how Bitcoin is helping the pot business.

Expect more Asian banks to launch video teller machines

Video banking will play an important role in the bank branch of the future.

Chart of the Week: Singapore banks' customer spreads 'stubbornly subdued'

They were 1.95 to 2.14% in Q1.

Check out how Singapore banks fare in terms of asset quality and pre-provision operating profit

Guess which bank posted the highest PPoP growth?

Weekly Global News Wrap Up: Here's why more people hate their banks; Morgan Stanley shuffles wealth unit

And HSBC partners with AI startup.

Singapore banks find profit in customers' wealth

Wealth management is showing great potential for the three biggest banks.

Singapore banks' profits to increase moderately over the next 12-18 months

Four factors will contribute to the modest growth.

Citi appoints Munir Nanji as global subsidiaries group head for Asia Pacific

He will be based in Singapore.

Thought Leadership Centre

In Association with

In Association with

Resource Center

Advertise

Advertise

Event News

New Charlton App ABF

It is a long established fact that a reader will be distracted by the readable content of a page when looking at its layout.